Source: ABL Advisor By: Michael A. Toglia

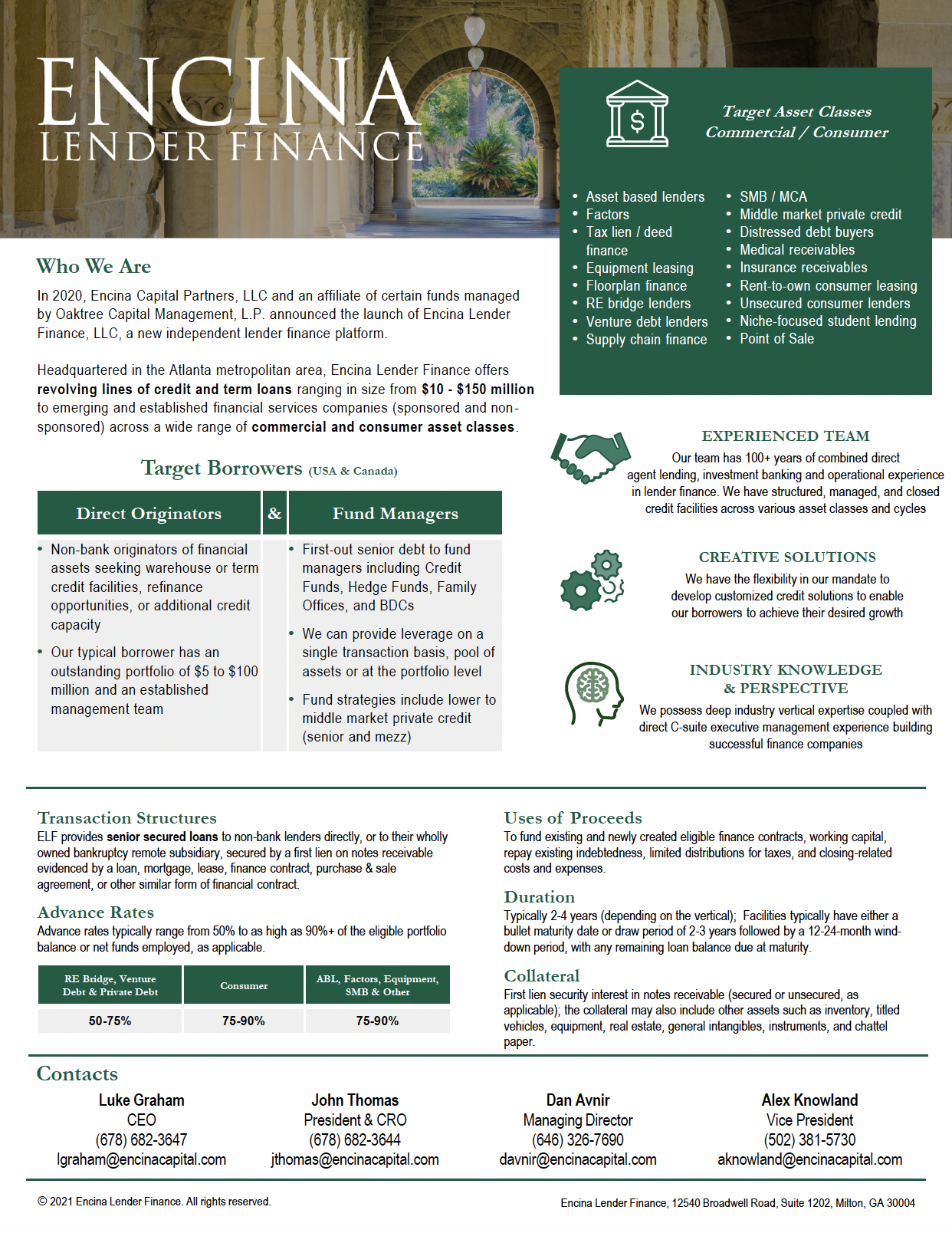

In the following interview, we catch up with Encina Lender Finance’s Chief Executive Officer, Luke Graham, and its President and Chief Risk Officer, John Thomas. It has been roughly 18 months since Encina Lender Finance’s launch, and we aim to explore how the pandemic, inflation, and a rising interest rate environment have influenced their strategy. ABL Advisor: How has the first full year in business gone? What have been the biggest challenges? Luke Graham: We completed a bit over $400 million in commitments, and just inside of $200 million in aggregate outstanding loan balance at the end of the year, so it was a big inaugural year. I’d say we had challenges like everyone in our industry, meaning we were coming off the COVID-19 pandemic in the beginning, and we operated lean and mean. We could have benefited from the addition of more staff in the early days. As a result, processes ran a bit slower which made transactions take longer to close. Another challenge we faced was that many of our third-party transaction providers, such as auditors, lawyers and so forth, had staff challenges throughout the year. There was a lot of demand and there were just not enough people available to allow processes to run as efficiently as they would have in a typical, normal environment. John Thomas: You can say it was a year of firsts. We launched the platform during the COVID-19 pandemic. There was a lot of uncertainty in the market about how banks were going to react, how law firms were staffed, and how the field exam firms were staffed. We couldn’t do onsite visits for example because people were unvaccinated, travel wasn’t available, and hospitality wasn’t available. It was a new environment where you couldn’t sit face-to-face with a CEO, a president, a CFO, and their teams to gain an understanding of their operations and how they were expecting to emerge from the pandemic. So again, it was a year of firsts, not just for the country, but for us as a lender. ABL Advisor: Overall, how would you say your investment thesis is playing out? Thomas: We’re hitting the marks and we’re on plan. We accomplished what we hoped to accomplish in our first year. As Luke mentioned, we closed a number of transactions, and we have a significant number of commitments at this time. We were well received in the market once we announced the launch, and outside of a bit of a learning curve because of the COVID environment, I think we did very well. Graham: I agree, and I would say we also hit important metrics related to the balance that we wanted to achieve in the portfolio. We hit the mark in terms of the types of transactions we thought we could win, and won our fair share. So, overall, it was a good outcome. ABL Advisor: What advantages does an independent finance company bring to the table versus banks providing lender finance products? Graham: First, our platform is focused on lender finance and lender finance only. Because we lend to both commercial finance companies and consumer finance companies, we have a very broad skillset, so we are not siloed like some of our competitors. We have a very broad mandate within those sectors. This enables us to pivot and do transactions where the opportunities present themselves, without tripping over some other group for example. I would say, the challenges we have is that if a transaction is in a sector that’s highly bankable, we’re not price competitive. We tend to focus on the higher yielding and smaller credits, where there’s less competition, or in sectors that are out of favor with some of the other larger players. Thomas: As a non-bank finance company, we can be flexible, more flexible than some other lenders. Additionally, I think it is important to mention that Luke and I have worked together for over 20 years in the lender finance space. Over the years, we’ve developed a strong reputation. We know most of the other players personally and have dealt with them either on the same side of the table or competed against them. We understand many asset classes and have a breadth of experience some of our competitors do not have. I believe this gives us a competitive advantage when we speak to a prospective borrower about their business – discussing what they do and how they do it – we can draw upon past experiences. Graham: I’d say there’s another component to this as well. We have relationships with bank and non-bank lender finance platforms, and we have a reputation of being a good shop with good people. As a result, we receive many referrals from our competitors on transactions that don’t fit their parameters. We also obtain a lot of great inbound referrals from people or institutions that we compete with in certain lender finance sectors – sectors where they or their institution are not actively lending. ABL Advisor: Tell us a bit about the team, the size of the team, its depth and how you work with the other parts of Encina. Graham: The way I think about Encina is we have our internal team focused on executing on ELF’s business plan. We also have our board, our investment committee (which is our credit committee), and people that are involved in the other Encina platforms. There’s great depth of experience in both groups, including experience setting up and running different types of finance platforms. These are people who have built very big and successful finance companies. They’ve been through numerous economic environments. This creates a culture that does not overreact to events or big shocks. Thomas: To Luke’s point, we have an excellent group of advisors on our board, with a tremendous amount of experience. From an operational standpoint and staffing the business for day-to-day operations, there was a bit of hesitation in the market to commit to join a startup coming out of the COVID environment as we were establishing ourselves. So, we were very lean initially. But as our portfolio and excitement for the platform have grown, we have staffed up. We now have ten people on the team in Atlanta, plus shared resources in Connecticut, with plans to hire at least five more team members later this year. Graham: When we launched the platform, we started with a dedicated staff of four and shared four or five resources from Encina Capital Partners. Then we hired people with more direct lender finance experience, and we continued this throughout the year, as we demonstrated success on the platform, and closed a number of deals. That’s part of having a playbook when you’re launching a new organization. We had the people with the skills that could handle the lender finance core business processes including John, myself, Alex Knowland, as well as Janet Riccard on our operations side. When it came to credit underwriting, John, Alex, and I have a tremendous amount of underwriting experience across a number of asset classes. Taken together, the four of us had the remaining fundamental skills necessary for success, documentation and deal closing experience, operations and treasury management experience and portfolio management. We were able to do business as a small and nimble team because we had the right team with the right skill set. Later we added people to contribute additional focus and depth to each discipline. We built the business through our team network, and we’ve been able to staff up in accordance with our plan. Today we have a team that’s focused on commercial finance company opportunities, and another team focused on consumer finance company opportunities. We have a strong plan, and we know what we need to do to continue scaling the business to our long-term goal of reaching $2 billion of funded portfolio in the next five years. ABL Advisor: As we enter a rising rate environment, how do you think the rising interest rates will impact business in 2022? Graham: In an increasing interest rate environment, it’s necessary to communicate with our borrowers in order to understand their plans. We provide floating rate debt so when rates rise, our rates go up. We do have clients with fixed rate products as well. I would say a rising rate environment increases the risk of recession, and I believe the Federal Reserve has a tough job ahead with respect to inflation rising as well. With our lender finance clients, we’re focused on making sure that they have a good pulse on what’s going on with their underlying borrowers and the challenges inflation and rising interest rates are going to have on them. If it’s a consumer finance company we must ask about what consumer segment they are focused on, if those consumers are feeling the pinch of inflation, if the lender will adjust its underwriting approach, and if they see opportunities to reprice. Additionally, we must learn what they are doing in terms of product design – meaning perhaps they are considering shortening the duration of their exposure to consumers so that they can reprice risk in a more efficient way. I would say rate increases beyond one percent are going to have an impact on lenders in general and I think in some cases rising interest rates will cause default rates to move up. Thomas: One of the things we’ve done is we’ve reached out to every one of our customers, given where the markets are going and the rising interest rates and asked them, what they are doing to prepare for rate increases. We want to know if they are being proactive and if they are evaluating their customer base. We also want to know what challenges they are anticipating in the upcoming year. We are taking a proactive approach, and we expect our customers to be doing the same. It’s critical to make sure our customers are taking all the appropriate steps to protect themselves going forward. Graham: One of the things we are also watching are unemployment rates. Wages are increasing and I believe commercial businesses are going to feel the pinch more because there’s going to be sectors that will become less profitable because wages are going up and input costs are also rising. Since commercial finance companies tend to have lower net interest margins, they will likely be impacted earlier if defaults rise due to economic pressures on their underlying borrowers. To respond to this, ELF will likely do slightly more consumer finance transactions in the near term where net interest margins are greater until we get a good sense of what’s going on with inflation and interest rates. We will be looking closely at delinquency trends within our client portfolio and will respond accordingly. ABL Advisor: Lastly, are you having fun? Graham: We really enjoy what we’re doing! We enjoy helping our clients. We’ve been dedicated to this market for a long time, and we’re going to continue to be dedicated to the lender finance space. We look forward to continuing to grow with our existing clients and hope to find many additional new clients over the next several years. We work hard to understand and listen to our customers and the challenges they face. We always try to be creative and supportive, and we are looking forward to having a successful year.